What Happens After a Total Loss Declaration in Georgia?

When an insurance company declares your vehicle a total loss, the claim can start moving very quickly. You may receive phone calls, emails, valuation paperwork, title instructions, and a settlement offer before you have had time to fully understand what just happened.

A total loss declaration usually means the insurance company has decided the vehicle is not economical to repair based on the value of the vehicle, the cost of repairs, the projected salvage value, and the terms of the policy.

But the declaration itself is only one part of the process. The bigger question is whether the settlement offer is accurate.

For drivers in Augusta, Central Georgia, Metro Atlanta, Athens, Gainesville, Rome, Ringgold, and surrounding communities, the most important thing to understand is this: a total loss declaration does not automatically mean the insurance company’s number is right.

If the valuation report uses weak comparable vehicles, misses important options, assigns the wrong trim, or applies unsupported condition adjustments, the final offer may not reflect the vehicle you actually owned.

Key point: The total loss decision and the settlement value are two different issues. Even after the vehicle is declared a total loss, the value should still be reviewed carefully before you accept the offer.

The Insurance Company Will Prepare a Valuation Report

After a total loss declaration, the insurance company usually prepares or orders a valuation report. This report is supposed to support the Actual Cash Value, often called ACV, of the vehicle immediately before the loss.

The report may look official, but that does not mean every detail is accurate. A valuation report is only as good as the information used to build it.

A proper review should look at the year, make, model, trim level, mileage, options, condition, accident history, local market data, and comparable vehicles used in the report.

Small mistakes can create a large difference. A missing technology package, incorrect drivetrain, wrong cab size, missing third row, incorrect mileage adjustment, or weak comparable vehicle can all reduce the final number.

Our guide on Actual Cash Value in Georgia explains how ACV should be reviewed and why the details behind the number matter so much.

You Will Receive a Settlement Offer

Once the valuation report is complete, the insurance company will usually present a settlement offer. That offer may include the vehicle’s Actual Cash Value, applicable taxes and fees, the deductible, the lienholder payoff if there is a loan, and any other adjustments that apply to the claim.

This is where many vehicle owners make a costly mistake. They focus on the final offer number without reviewing how that number was created.

Before accepting a settlement, request the full valuation report and compare it against your actual vehicle. Look at the trim, mileage, equipment, condition ratings, comparable vehicles, and deductions.

If the offer seems too low, do not assume the number is final just because it came from the insurance company. Our related guide on Total Loss Offer Too Low in Georgia explains common valuation problems that can reduce a settlement offer.

A settlement offer should make sense on paper. If the report does not support the number, the offer may need a closer review.

Check the Comparables Before You Agree

Comparable vehicles are one of the most important parts of a total loss valuation. These are the vehicles the report uses to help determine what your vehicle was worth before the accident.

The problem is that not every comparable is truly comparable.

A vehicle may be the same year, make, and model but still be very different from yours. It may have a lower trim level, fewer options, higher mileage, different drivetrain, weaker condition, or a price that does not reflect the real local market.

When the comparables are weak, the value can be pulled down. When the vehicle details are incomplete, the offer can be lower than it should be.

Common comparable vehicle problems include:

- Wrong trim level or package

- Missing factory options

- Higher mileage vehicles used against your lower mileage vehicle

- Vehicles listed outside a reasonable market area

- Dealer listings that are not truly similar

- Condition adjustments that are not clearly supported

- Prior damage or history issues in the comparable vehicles

Key point: A valuation report should compare your vehicle to vehicles that are truly similar, not just vehicles that share the same basic nameplate.

What If You Still Owe Money on the Vehicle?

If there is a loan on the vehicle, the lender usually has to be paid from the settlement. This can create confusion because the settlement is based on the vehicle’s value, not necessarily the amount still owed on the loan.

If the loan payoff is lower than the settlement amount, the remaining balance may go to the vehicle owner after the lender is paid. If the loan payoff is higher than the settlement, the owner may still owe money unless GAP coverage or another protection applies.

This is one reason an accurate total loss valuation matters. A low settlement offer can create a larger financial problem when a lienholder is involved.

Before signing settlement documents, make sure you understand the ACV, deductible, payoff amount, taxes, fees, and any deductions being applied.

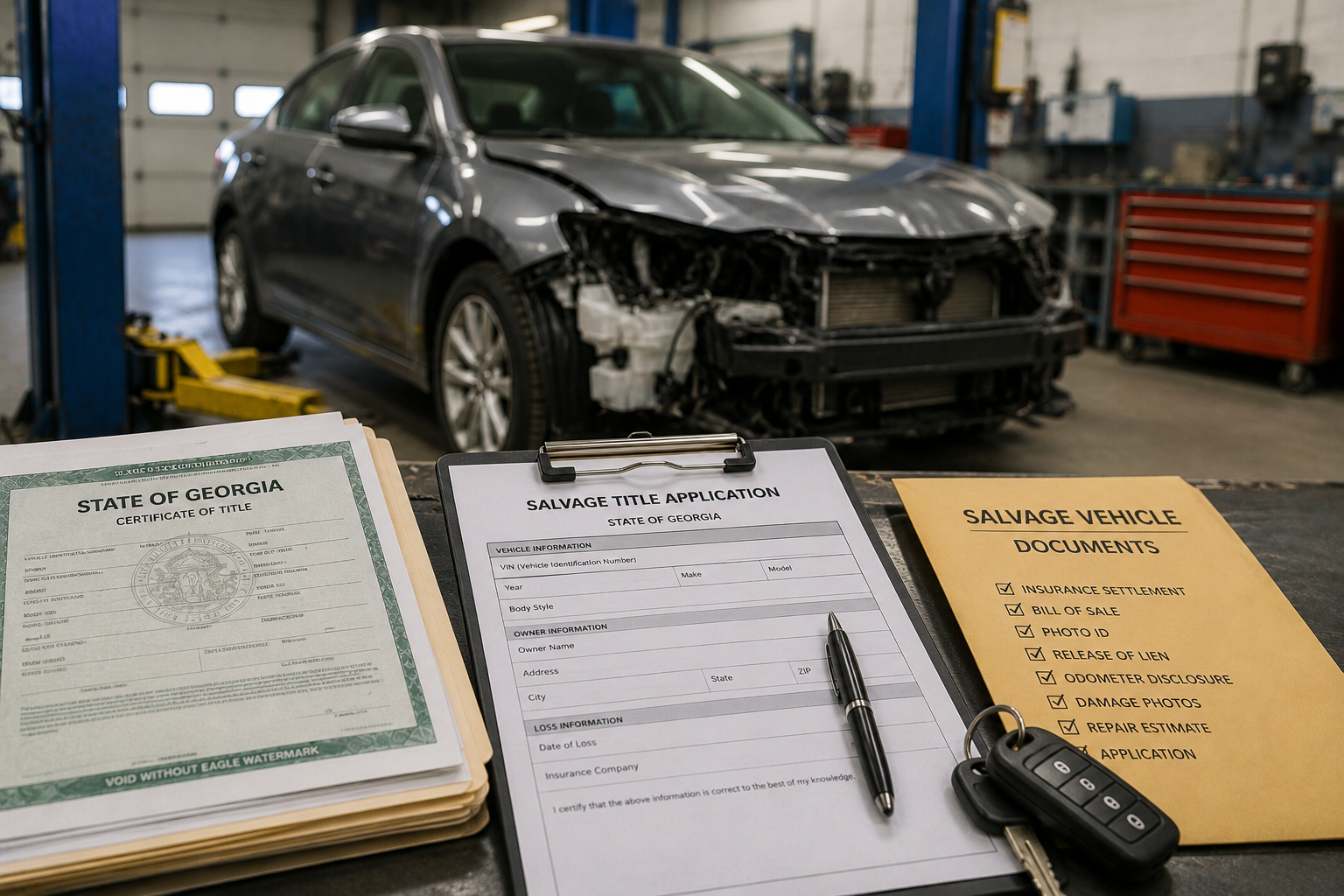

What Happens to the Title After a Total Loss?

The title process depends on what happens to the vehicle after the settlement. If the insurance company takes the vehicle as part of the total loss settlement, title paperwork usually moves toward the insurance company and the salvage process.

If you decide to keep the damaged vehicle, the process can become more complicated. This is often called retaining salvage or owner retained salvage.

Keeping the vehicle may reduce the settlement by the salvage value. It may also create title, inspection, repair, resale, and insurance issues that should be understood before you agree.

In Georgia, a salvage vehicle is not simply a regular vehicle with damage. A salvage title can affect whether the vehicle can be driven, sold, repaired, inspected, insured, or later titled as rebuilt.

Before keeping a totaled vehicle, make sure you understand what documents are required, what deadlines apply, and what the vehicle will need before it can legally return to the road.

Can You Keep the Vehicle After a Total Loss?

Some vehicle owners want to keep the damaged vehicle after a total loss. This may happen because the vehicle has sentimental value, the owner believes it can be repaired, or the owner wants to use it for parts.

That decision should be made carefully.

If you retain the vehicle, the insurance company may subtract the salvage value from the settlement. That means you may receive less money because you are keeping the damaged vehicle instead of turning it over to the insurance company.

You also need to think beyond the settlement number. A retained salvage vehicle may require title steps, proper repairs, inspections, and rebuilt title approval before it can be legally operated again.

Questions to ask before keeping the vehicle include:

- How much salvage value is being deducted from the settlement?

- Will the vehicle require a salvage title?

- What repair documentation will be needed?

- Can the vehicle pass the required inspection process?

- Will the vehicle be insurable after repairs?

- Will the branded title affect future resale value?

If the salvage deduction seems high or the total settlement does not make sense, review the valuation before agreeing to the retained salvage terms.

When the Appraisal Clause May Matter

If the disagreement is about the value of the vehicle, your policy may contain an appraisal clause that can help resolve the dispute.

The appraisal clause is not for every situation. It generally applies when the loss is covered, but the vehicle owner and insurance company disagree about the amount of the loss.

In a total loss claim, this may involve the Actual Cash Value, comparable vehicles, condition adjustments, mileage adjustments, options, or other valuation details.

Our guide on the Auto Insurance Appraisal Clause in Georgia explains when the process may apply and how independent appraisers can help resolve a valuation dispute.

Common Mistakes After a Total Loss Declaration

The total loss process can feel rushed, and that pressure often causes people to accept terms before they understand the full impact.

Some mistakes are simple. Others can affect the settlement amount, the title process, the loan payoff, or the ability to challenge a low valuation later.

Common mistakes include:

- Accepting the first offer without reviewing the valuation report

- Failing to confirm the correct trim level and options

- Ignoring mileage, condition, or comparable vehicle errors

- Assuming the insurance company’s value is automatically correct

- Not understanding how the deductible was applied

- Not checking whether taxes and applicable fees were included correctly

- Keeping the salvage vehicle without understanding title requirements

- Overlooking the loan payoff and possible GAP coverage issue

- Waiting too long to ask questions about the offer

- Signing settlement documents before getting an independent review

The best time to ask questions is before the settlement is finalized. Once paperwork is signed and the title process moves forward, correcting mistakes can become more difficult.

Before You Sign, Have the Settlement Reviewed

A total loss declaration can create pressure, but you still deserve clear answers before accepting the settlement.

Collision Safety Consultants of Central Georgia reviews total loss valuation reports, comparable vehicles, settlement details, options, mileage, condition adjustments, and documentation so drivers can better understand whether the offer appears reasonable.

The goal is clarity. Before you sign away rights, surrender a title, accept a salvage deduction, or agree to a settlement number that does not make sense, get the details reviewed.

Serving Drivers Across Georgia

Collision Safety Consultants of Central Georgia works with drivers throughout Augusta and Central Georgia, as well as Metro Atlanta, Athens, Gainesville, Rome, Ringgold, and surrounding communities.

Request Your Total Loss Review Today

If your vehicle has been declared a total loss, do not accept the settlement blindly. Get help reviewing the valuation, the comparables, the settlement details, and the next steps before you make a final decision.

Total Loss Declaration in Georgia

Questions & Answers

A total loss declaration usually means the insurance company has decided the vehicle is not economical to repair based on the damage, repair cost, vehicle value, salvage value, and policy terms. That does not automatically mean the settlement offer is correct.

Not until you have reviewed the valuation report. The first offer may be based on incorrect comparable vehicles, missing options, wrong trim information, unsupported condition deductions, or incomplete market data.

Review the year, make, model, trim level, mileage, options, condition, comparable vehicles, local market prices, taxes, fees, deductible, and any deductions. Our guide on Actual Cash Value in Georgia explains these details more fully.

Yes. If the dispute is over the value of the vehicle, the valuation can often be reviewed and challenged with better documentation. If your offer seems low, read our guide on Total Loss Offer Too Low in Georgia.

If there is a lienholder, the lender is usually paid from the settlement first. If the settlement is less than the loan payoff, you may still owe the difference unless GAP coverage or another protection applies.

In some cases, yes. This is often called owner retained salvage. If you keep the vehicle, the insurance company may subtract the salvage value from your settlement, and Georgia salvage title requirements may apply.

No. A salvage vehicle cannot be legally operated on public roads in Georgia. Before it can return to the road, it generally must go through the proper repair, inspection, and rebuilt title process.

If your policy includes an appraisal clause and the disagreement is about vehicle value, the appraisal process may help resolve the dispute. Learn more in our guide on the Auto Insurance Appraisal Clause in Georgia.